1300 628 071

1300 628 071

Climate-aware investing

Climate risks and opportunities

The green transition

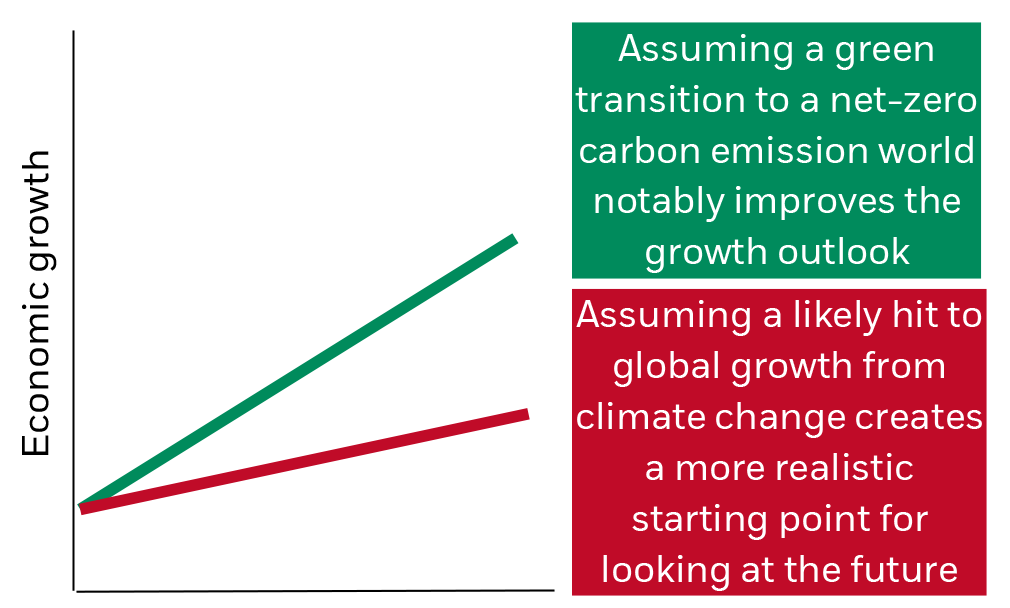

Climate change and efforts to curb it will have major economic outcomes, we believe, not just far into the future but even in the next five years. Economic projections that ignore climate change are widely relied upon – yet are based on an unrealistic future scenario, in our view. The two scenarios to compare from this perspective: a transition to a low-carbon economy in which policies to fight climate change are enacted, and a no-climate-action scenario with no actions to limit damages.

A commonly held notion is that tackling climate change has to come at an economic cost. We think that’s wrong. We assume the global economy transitions to a lower carbon path consistent with Paris Agreement goals. The positive effect of this transition rests on a gradual phasing in of carbon taxes, green infrastructure spending consistent with the IMF’s recommendation, and subsidies on renewable energy. If none of these actions are taken to mitigate climate change, we estimate a cumulative loss in global output of nearly 25% in the next two decades. The stylized Accounting for climate change chart illustrates the potential difference between the two paths.

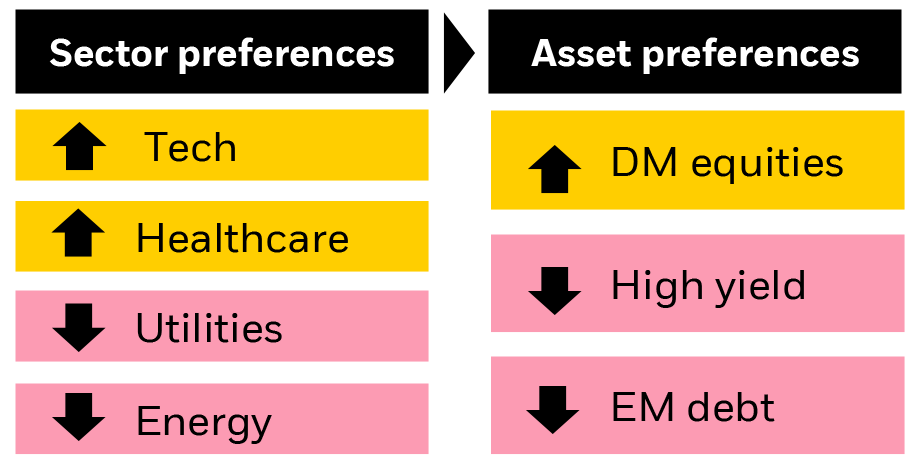

Climate change will drive dispersion of returns at a sector level, in our view. There will be sectoral winners and losers – underpinning why we believe a sectoral approach to sustainable investing is more appropriate than a regional one. Likely beneficiaries are technology and healthcare, we believe, while laggards include energy and utilities.

We focus on the "E" (environmental) of ESG in our updated CMAs. Why? First, there is wide recognition of the importance of climate change on economic and social outcomes. Second, there is consensus on the measurement of an entity’s contribution to climate change: carbon emissions. Carbon emissions have become a widely enough adopted indicator of sustainability for investors to be a driver of repricing at the broad market level.

We see insights into S (social) and G (governance) as key sources of potential returns through security selection, rather than as systematic drivers of returns. We will consider incorporating them in our framework once consensus around their impact and availability of consistent data improve in coming years.

“We see a green transition as a positive for growth and risk asset returns.”

Natalie Gill

Portfolio strategist,

BlackRock Investment Institute

Accounting for climate change…

Stylized illustration of global growth paths

Source: BlackRock Investment Institute, February 2021. Notes: This is a stylized depiction of our best estimate of how we believe global growth will evolve in two scenarios, based on information currently available. It is not intended to reflect the size of the potential difference between the two paths. There is no guarantee that a positive investment outcome will be achieved.

…leads to a change in views

Impact of climate-aware CMAs on our views

Sources: BlackRock Investment Institute, February 2021. Notes: This is a stylized depiction of our sectoral and asset class preferences on a strategic horizon as a result of incorporating climate change in our capital market assumptions. They are not meant as investment advice or an investment recommendation. There is no guarantee that a positive investment outcome will be achieved.

How does all of this translate into our strategic views? There are broad differences between our new, climate-aware views versus those based on scenarios that ignore climate change or assume no mitigation. See the table.

Our preference for DM equities has become stronger, at the expense of high yield and some EM debt. Why? The composition of DM equity indexes better aligns with the climate transition, with large weights of technology and healthcare companies, less vulnerability to transition risks and lower carbon intensity. Equities also can better capture potential opportunities of the green transition, as bonds are capped in their capital appreciation.

Incorporating climate change

The climate framework

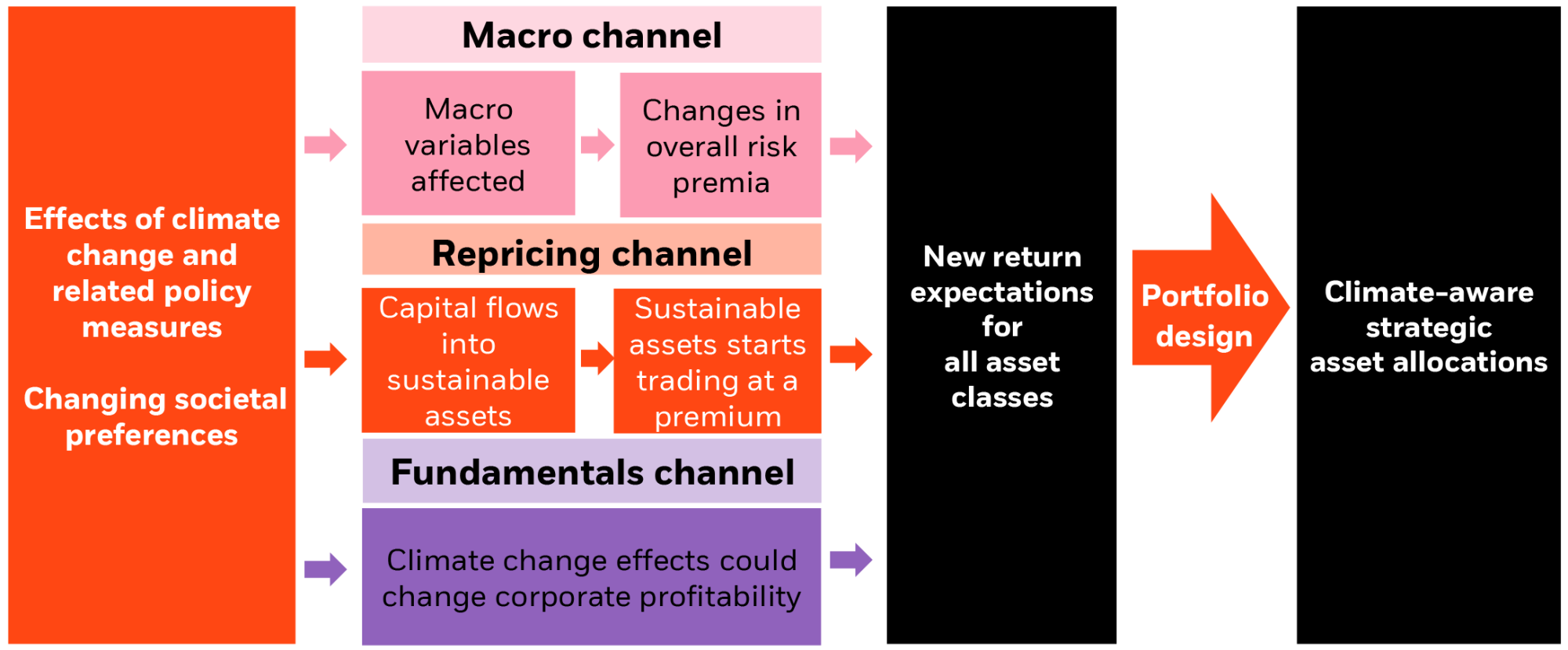

Our framework, illustrated in the schematic below, outlines how we incorporate climate change and shifting investor sustainability preferences into expected asset class returns and, ultimately, strategic asset allocation. We see climate change entering the equation through three channels: macro, repricing and fundamentals.

Macro:

We believe macro variables will be different in a world that is transitioning to a sustainable future. Such changes mean sustainability affects everything that goes into forming a view on long-term asset class returns. We see changes in so-called risk premia for all asset classes – the compensation investors require for holding them.

Repricing:

The price investors are willing to pay for sustainable assets is changing. The BlackRock Global Sustainability Survey of September 2020 found 425 institutional investors planned to double their sustainable assets under management in the next five years to 37%. We see this as a tectonic shift toward sustainable assets. Changing investor preferences will spur a climate change-led repricing due to the falling cost of capital for sustainable assets. These assets will generate higher returns than traditional peers as a result, in our view. Investors are just starting to respond to the structural shift, suggesting it is not yet in the price. Once this repricing phase has passed, we believe this channel will eventually no longer be this channel is no longer a boon for "greener" assets' expected returns.

Fundamentals:

Climate change and policies will affect profitability across sectors, we believe. This will have knock-on effects for other variables such as credit default and downgrade assumptions. We estimate corporate earnings consistent with our green transition scenario. To arrive at estimates, we first assess the sensitivity of earnings to carbon pricing. We then assess the impact of transition risks – or the financial risks arising from the transition to a low-carbon economy – and physical risks.

We score sectors on two dimensions: How exposed they are to climate change, and whether that exposure represents a risk or opportunity. For example, a company could be a high carbon emitter and have a high carbon price sensitivity as a result, yet still benefit from the green transition. Think of chemical companies that manufacture materials for electric vehicle batteries.

No one knows yet what a low-carbon world will look like. Climate change projections are highly uncertain. This is due to the complexity of modelling the dynamics and myriad dependencies between climate and carbon emissions, economic variables and mitigation policies.

Our framework allows us to systematically monitor key metrics and the evolution of the green transition, and we plan to adapt it accordingly. Our approach explicitly accounts for uncertainty - highly relevant for climate change that will have varying but highly uncertain impacts over time. We believe this approach lends itself well to the structural transformation taking place.

Three channels drive the climate change impact on assets

BlackRock framework for climate-aware portfolios

Source: BlackRock Investment Institute, February 2021. Notes: For illustrative purposes only. Subject to change without notice.

BlackRock Investment Institute

The BlackRock Investment Institute (BII) leverages the firm’s expertise and generates proprietary research to provide insights on the global economy, markets, geopolitics and long-term asset allocation – all to help our clients and portfolio managers navigate financial markets. BII offers strategic and tactical market views, publications and digital tools that are underpinned by proprietary research.

BlackRock’s Long-Term Capital Market Assumption Disclosures: This information is not intended as a recommendation to invest in any particular asset class or strategy or product or as a promise of future performance. Note that these asset class assumptions are passive, and do not consider the impact of active management. All estimates in this document are in US dollar terms unless noted otherwise. Given the complex risk-reward trade-offs involved, we advise clients to rely on their own judgment as well as quantitative optimisation approaches in setting strategic allocations to all the asset classes and strategies. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Assumptions, opinions and estimates are provided for illustrative purposes only. They should not be relied upon as recommendations to buy or sell securities. Forecasts of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. If the reader chooses to rely on the information, it is at its own risk. This material has been prepared for information purposes only and is not intended to provide, and should not be relied on for, accounting, legal, or tax advice. The outputs of the assumptions are provided for illustration purposes only and are subject to significant limitations. “Expected” return estimates are subject to uncertainty and error. Expected returns for each asset class can be conditional on economic scenarios; in the event a particular scenario comes to pass, actual returns could be significantly higher or lower than forecasted. Because of the inherent limitations of all models, potential investors should not rely exclusively on the model when making an investment decision. The model cannot account for the impact that economic, market, and other factors may have on the implementation and ongoing management of an actual investment portfolio. Unlike actual portfolio outcomes, the model outcomes do not reflect actual trading, liquidity constraints, fees, expenses, taxes and other factors that could impact future returns.

Capital at risk. The value of investments and the income from them can fall as well as rise and are not guaranteed. Investors may not get back the amount originally invested.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation or an offer or solicitation to purchase or sell any securities, funds or strategies to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The opinions expressed are as of February 2021 and are subject to change without notice. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks

In Australia, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975 AFSL 230 523 (BIMAL). The material provides general information only and does not take into account your individual objectives, financial situation, needs or circumstances.

© 2021 BlackRock, Inc. All Rights Reserved. BLACKROCK is a registered trademark of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.